THE REPUBLIC OF CYPRUS AGREES ON AMENDMENTS TO THE DOUBLE TAXATION AVOIDANCE TREATY PROPOSED BY RUSSIA

The following changes took place in the tax area:

1. Russian Federation and the Republic of Cyprus agreed to amend the Treaty on the avoidance of double taxation in regard to 15% withholding tax on the payment of dividends and interest at the source;

2. the Ministry of Finance postponed cancellation of the “pass-through approach” to taxation of dividends until 2024. The President's appeal to the Russian citizens on March 25, 2019 entailed reconsidering legislative regulation in terms of taxation of income from sources in the Russian Federation paid abroad. As part of this appeal, the Government of the Russian Federation was assigned to amend the existing agreements on the avoidance of double taxation so that income in the form of dividends received abroad would be taxed at a rate of at least 15% at the source of payment.

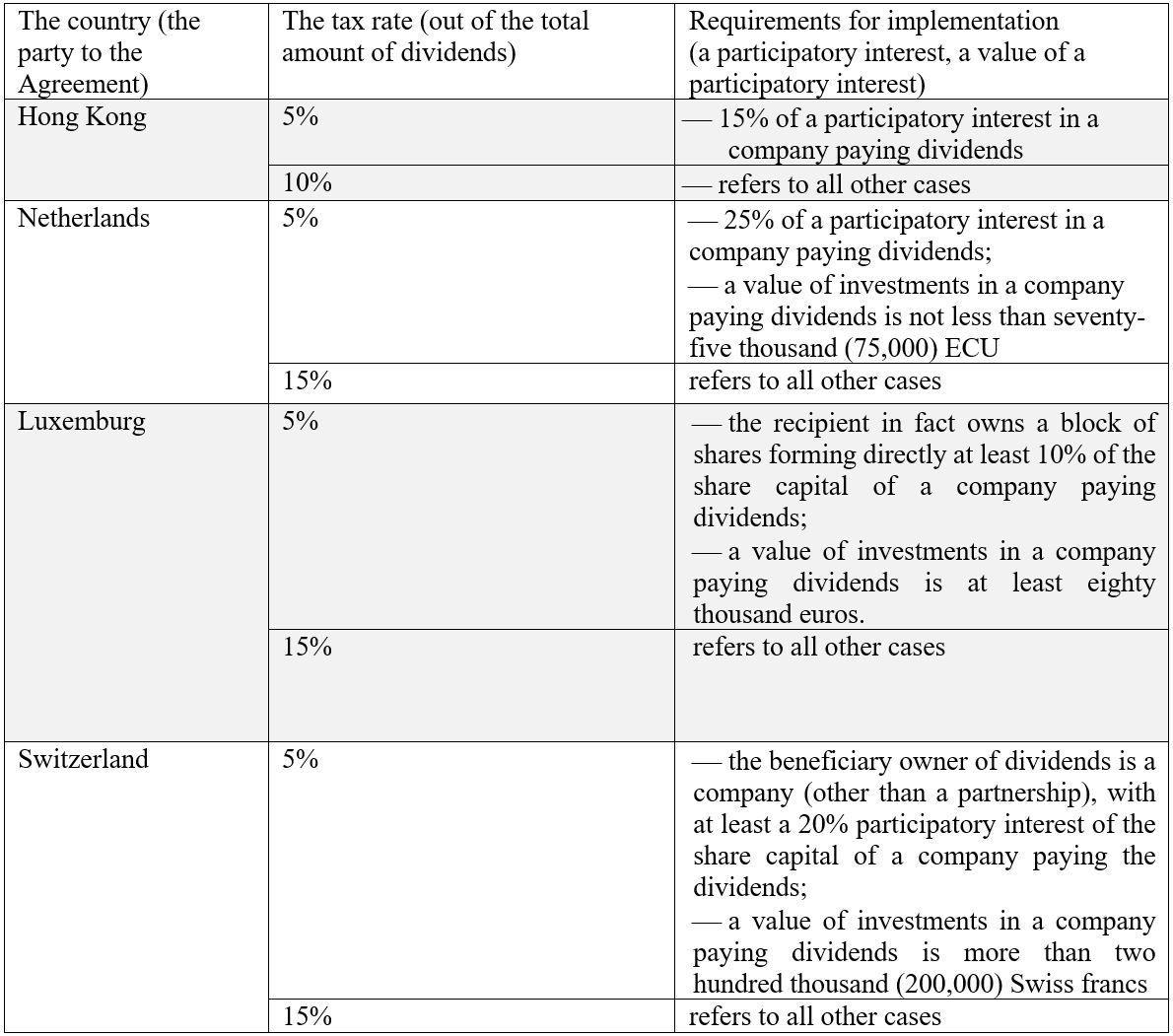

1. Amendments to effective agreements on the avoidance of double taxation While performing the President’s assignment the Government of the Russian Federation focused on the most popular jurisdictions that are used to apply preferential tax rates. First of all, it refers to the Republic of Cyprus, the Ministry of Foreign Affairs of which was the first (March 31, 2020) to announce the receipt of the letter from the Ministry of Finance of the Russian Federation with a proposal to alter the effective Treaty between the Government of the Russian Federation and the Government of the Republic of Cyprus on the avoidance of double taxation with respect to taxes for income and capital dated December 5, 1998 (hereinafter - the Treaty with Cyprus). Subsequently (April 13, 2020), the letters were sent to the relevant ministries of the Grand Duchy of Luxembourg and the Republic of Malta[1]. The next step is likely to be the reconsideration of the relevant agreements with Hong Kong[2] and Switzerland[3], as it was announced during the meeting of the President with members of the Government dated August 11, 2020[4]. Negotiations with Malta were meaningful, and it was announced that amendments’ protocol to the current Convention between the Government of the Russian Federation and the Government of Malta for the avoidance of double taxation and the prevention of tax evasion with respect to taxes on income was approved on August 13, 2020. The Convention allows the tax rate on dividends to be reduced up to 10% or even up to 5% provided that the recipient of the dividend has a 25% of a participatory interest in the company paying the dividend and the value of such a participatory interest is at least 100,000 EURO. After the enforcement of amendments income in the form of dividends will be taxed at source at the rate of 15%, with the exception of certain institutional investments[5]. On August 5, 2020 the Kingdom of the Netherlands also received a proposal to reconsider the current Treaty between the Government of the Russian Federation and the Government of the Kingdom of the Netherlands dated 12.16.1996 “On the avoidance of double taxation and prevention of tax evasion with respect to taxes on income and property”. The negotiation process between the authorized departments of Russian Federation and the Republic of Cyprus was difficult and protracted, the parties could not come to an agreement for a long time, and initially the Ministry of Finance announced the denunciation of the Treaty with Cyprus starting from August 03, 2020, however, on August 10, 2020, the press center of the Ministry of Finance published a message that the party of the Republic of Cyprus agreed with the proposed conditions, and the denunciation process was suspended. The effective Treaty with Cyprus provides for special legal regulation for the taxation of various types of income, including income in the form of dividends and interests (interests refers to income from debt claims of any kind, in particular, income from government securities, bonds or debt obligations). According to current regulation, if a company registered in the Republic of Cyprus receives income from Russia, then dividends paid by such Cypriot company cannot be taxed in Russia if they are paid to a Cypriot resident (Para. 5 of Art.10 of the Agreement with Cyprus). If a recipient of dividends paid by such an “intermediate” Cypriot company is in fact a tax resident of Russia, the dividends are taxed at a rate not exceeding: ¾ 5% of the total amount of dividends, provided that a participatory interest in the company paying the dividends is at least 100,000 EURO; ¾ 10% in all other cases. Interests are not taxed at the source of payment, i.e. if interests arise in Russia and are paid to a Cypriot resident, they are taxed only in the Republic of Cyprus. The Ministry of Finance proposed to increase the rate at which dividends and interest are taxed up to 15%, which was initially rejected by the representatives of the Republic of Cyprus. If the Treaty with Cyprus was denounced, the tax on dividends paid by Russian companies would be withheld twice: at the source in Russia upon payment, and then in Cyprus. By accepting the proposals of Russia, the Republic of Cyprus found itself in a more advantageous position than it would be if the agreement had been terminated. Pursuant to the proposed alterations: ¾ tax at sources on dividends and interests will be increased up to 15%; ¾ for pension funds, insurance organizations, as well as some other organizations (more detailed information is expected at a later date), the tax rate will be equal to 5 or 0%[6]. As a result, businesses entities will be forced to look for new approaches to construct their economic activities, for example, to carry out re-domiciliation, which means to change the jurisdiction to Russian or another one that has an effective agreement on avoidance of double taxation with Russia. In case of a transition to the Russian jurisdiction, there is an opportunity to take advantage of preferential tax regimes provided for special administrative regions: the territory of Russkiy Island (Primorskiy Territory) or Oktyabrskiy Island (Kaliningrad Region), however, this requires the presence of an international holding company in the structure, for registration and activities of which a number of requirements are imposed in accordance with the Federal Law № 290-FZ “On international companies and international funds” dated by August 3, 2018. All of the aforementioned double taxation agreements, which are currently being reconsidered or planned to be reconsidered, also provide taxpayers with very favorable conditions. Almost all agreements completely exempt interests’ taxation at source. Reduced tax rates are provided for the tax on dividends provided that the recipient of dividends has certain shares in a foreign company that pays dividends.

2. Application of “pass-through” taxation of dividends Reconsideration of agreements on avoidance of double taxation is not the only measure to prevent transfer of assets to foreign jurisdictions on preferential terms. Taxpayers can currently apply the so-called “pas-through approach”. Current version provides for an opportunity to apply zero tax rate (supara. 3 para. 1.1 art. 312 of the Tax Code of the Russian Federation) on dividends received by a foreign company if such company states that the actual dividend recipient is a tax resident of the Russian Federation. Therefore, such income paid to “transitory” jurisdictions, but the actual recipients of which are Russian residents, is not taken into account for taxation purposes. Such right arises if: ¾ the indirect participation of a Russian resident who is actually entitled to dividends is not less than 50%; ¾ the amount of dividends that are paid to a Russian resident is not less than 50% of the total sum of distributed dividends. The Ministry of Finance prepared a draft of the Federal Law “On the introduction of amendments to the first and second part of the Tax Code of the Russian Federation concerning implementation of certain provisions of budgetary, tax and customs tariff policy of the Russian Federation”. Such amendments exclude the right to apply zero tax-rate on dividends paid to a foreign company if the actual recipient of such dividends is a Russian resident. If the draft law is adopted, the tax rate on dividends received by a foreign company at the source in Russia shall be strictly 13%. The draft law cancelling “pass-through” approach was sent to the Government but under the information provided by the press-office of the Ministry of Finance to a publishing house[1], its adoption cannot be expected until December 31, 2023. Both of the above measures are aimed at the recovery of funds in the form of dividends paid to foreign jurisdictions. At the same time, “pass-through” approach is not so widespread, therefore, presumably, its cancelation would not have had a significant impact on the amount of fiscal revenues. The new version of the Treaty with Cyprus is expected to enter into force after January 1, 2021[2]. However, the Ministry of Finance has already declared that the fiscal revenue will amount to 150 billion rubles a year as a result of amendment of the Treaty with Cyprus.